Generally one has two choices when responding to the question, How are you?” The conventional option is to simply respond, Fine. How are you?” and move on with life. The other choice is to respond honestly in some long, drawn-out monologue for which nobody really has the time or interest to hear. Often honest to a fault, I sometimes take the less conventional route and bore my friends to death.

The truth is that I am mostly doing great. I couldn’t be happier about my family, friends, and financial security. Regarding health: I am feeling the creaks in my body commensurate with my age (which could be rounded up to 50 – Yikes!), but this is nothing to complain about given my general good fortune.

The one thing that compels me to answer the How are you?” question with a more descriptive long-form, however, is interest rates. They are at rock bottom lows. The ten-year US Treasury rate is around 1.5%, and rates are negative in Japan, Germany, and Switzerland. So, What’s the problem? That means that mortgages and car loans are cheap!” you may be thinking. The problem is that history suggests low interest rates mean low portfolio returns. Everything is based off of interest rates; not just the loans you receive but also the expected returns on your capital. The prospect for low investment returns is a bit less uplifting than other elements of my life.

But this is a hard truth I believe we must face. On average stocks have made only around 5% to 7% more than short-term US Treasury bond yields. With short-term government bonds having yielded little more than 0% since December 2008, history seems to suggest we are in for stock market returns well below the long-term average. Moreover, with interest rates at unprecedented lows, high quality bonds are likely only to dampen risk while serving as a heavy drag on portfolio returns.

With lower returns on the horizon individuals are faced with two options to meet previously defined financial goals: 1) reduce expenses/modify goals or 2) increase risk. Of course, nobody likes to reduce expenses or sacrifice the second home, so many choose to increase risk.

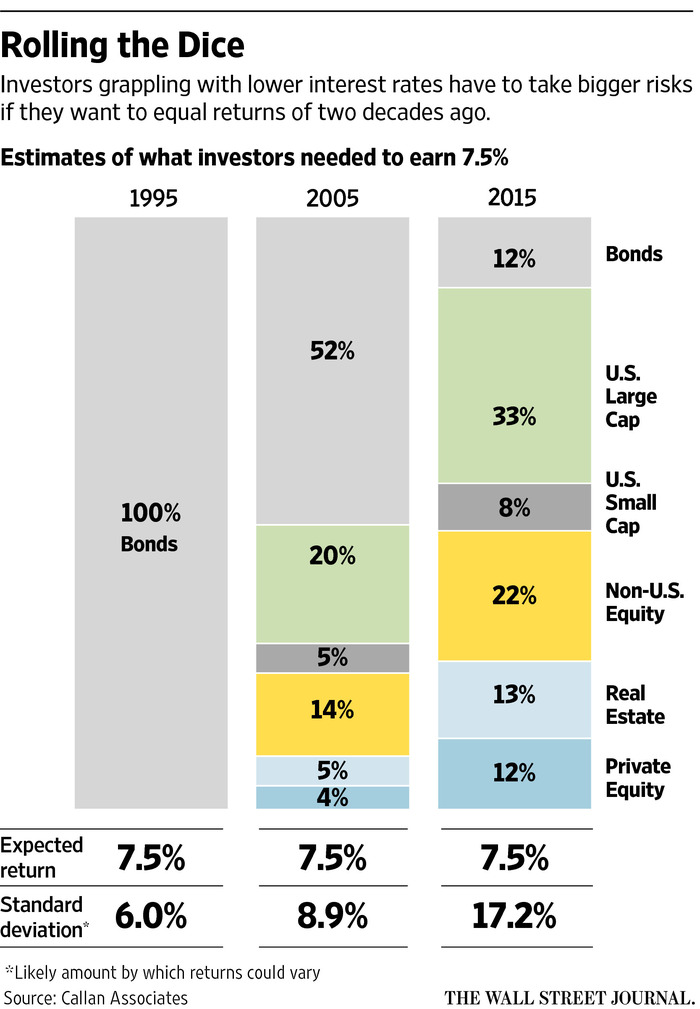

But do people really know what this means? Recently Callan Associates, one of the more legitimate investment consulting firms to pensions and endowments, released a study comparing the kinds of risk one must take now vs. ten and twenty years ago in order to make a seemingly reasonable 7.5% annual return. (See the chart to the right.) Twenty years ago, one could make 7.5% while sitting in the safety of a 100% bond portfolio. In order to make 7.5% now, Callan suggests that one would have to invest nearly 90% of one’s portfolio into risky assets, including illiquid real estate and private equity investments. Such a portfolio is estimated to be around three times riskier” (vis-Ã -vis the standard deviation measure of volatility and therefore risk) than the 100% bond portfolio. This is unnerving to say the least.

I share these fun facts” not because I want to send my beloved clients into fits of depression. After all, the political forces of today would be hard to trump in that regard. I share because I care. After all, with knowledge comes power. You have a financial advisor with many investment and planning tools in the shed; we are not powerless even in the current environment. First of all, through financial planning we can identify how much return one should really need. Then, we can talk about risks one is willing to take to increase the odds for higher returns. If these risks don’t sit well, or the returns don’t float the boat, then we can talk about how inflationary your lifestyle may be or areas of your lifestyle that you may be willing to cut back to improve security.

Hmmm. I am glad I got all this off my chest; I feel better already. If nothing else, now you know not to ask me How are you?” unless you have a moment and want the honest truth!