As a student (especially for us self-proclaimed nerds!), it seemed as though your GPA had the ability to dictate the course of your life – what college you were accepted into, what your major was, what job you were offered, etc. While a good GPA certainly doesn’t hurt, it isn’t quite the determining factor it once appeared to be. However, turns out that there’s another score that actually can have a meaningful impact, at least financially…

Your credit score is used to rate your risk as a borrower, and landlords, lenders and potential employers may look to your credit score as an indicator of financial responsibility. This can affect your ability to rent an apartment, the interest rate on your mortgage and even your career opportunities. As an example, the interest rate on a mortgage could be a full percentage point higher for someone in the lowest credit tier (550 and below) than for someone in the highest credit tier (750 and above). For a $400K mortgage this would result in more than $100K of additional interest over the life of a 30 year loan!

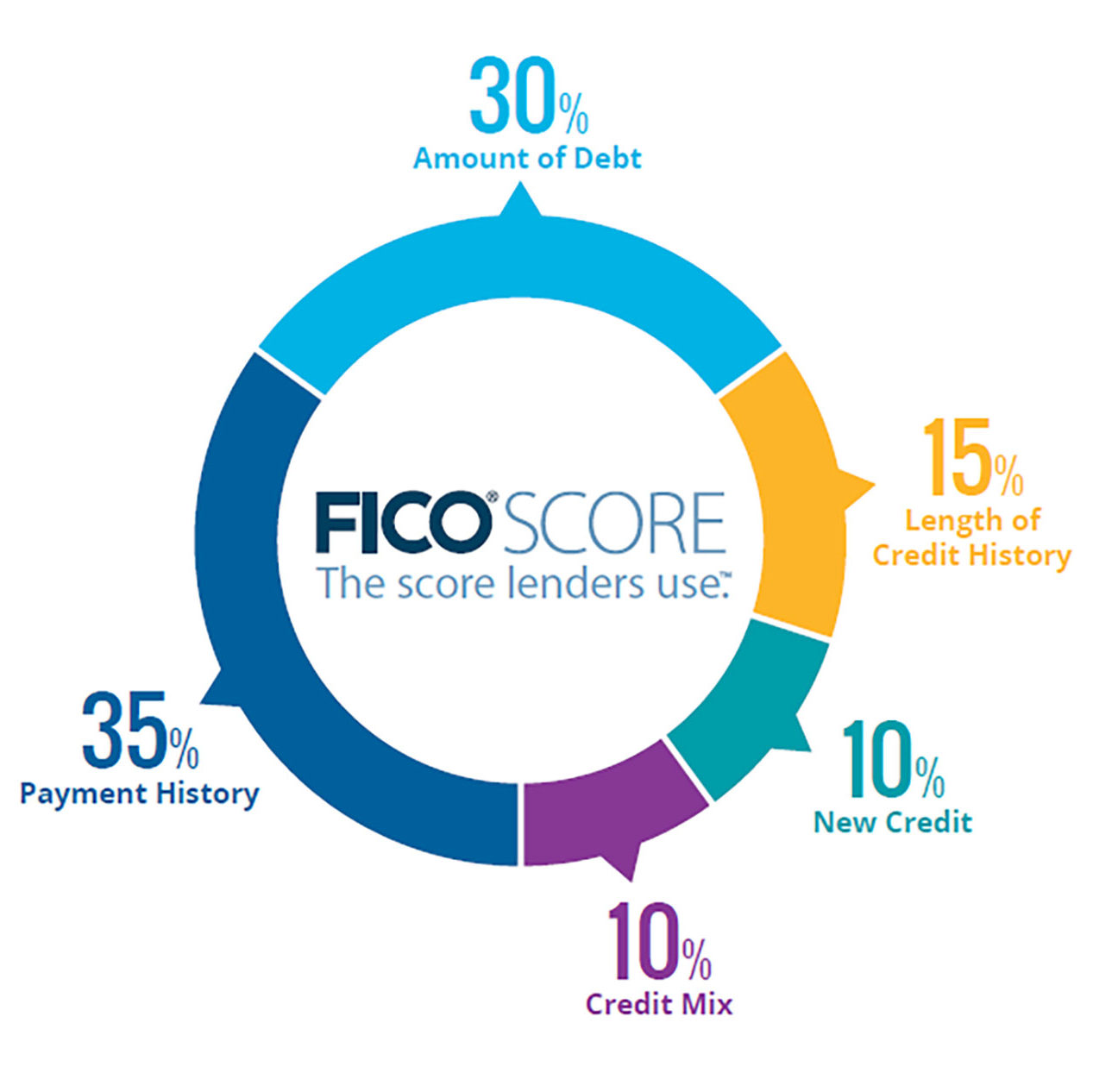

Despite the potential bearing on our lives, credit scores still seem to be a puzzle to many and I’ve had numerous conversations with clients and friends on how exactly credit scores are calculated and what factors truly influence your score. Below I take a more detailed look at some common questions:

Does checking my credit report reduce my score?

You may be reluctant to run your credit report because you’ve heard that too many inquires can lower your score. While numerous inquiries from lenders (hard inquiries”) in a short period of time can result in a temporary – often minimal – drop in your score, running your own report is considered a soft inquiry” and has no impact on your score. In fact, keeping an eye on your report (we recommend checking at least once a year) allows you to check for errors and resolve any discrepancies.

How many is too many?

A group of us had a debate a few weeks ago about the right” number of credit cards. We pulled out our wallets and counted how many cards we each had – it ranged from three to twelve. So is there a right” number?

No. The ideal number is going to differ from person to person. Having more cards can help with your credit utilization ratio – your total current debt balance vs. your total credit limit among all of your cards since more cards means more available credit. But that doesn’t mean opening a credit account you don’t need. More cards also means more accounts to track, more annual fees and an increased likelihood of a payment slipping through the cracks. A missed payment would negate any benefit the additional credit limit provided to your score.

However, it does help to have a mix of credit account types. Revolving accounts, such as credit cards and lines of credit, have different payment amounts every month depending on your usage while installment accounts, such as a mortgage or auto loans, have a fixed payment amount every month depending on the term and rate of the loan. Open accounts, such as utility and cell phone bills, have to be fully paid off each month and don’t typically involve interest charges. There’s no magic ratio with the various types of credit accounts but having a mix of all three is a testament to the willingness of different lenders as well as your financial responsibility and experience.

Should I close accounts I no longer use?

With a new credit card offer in the mail every day and tempting rewards and bonus points, it’s easy to end up with a card or two that you obtained for a specific purpose but don’t really use. Does it make sense to close these?

Closing accounts can actually cause a drop in your score since your total available credit limit decreases and therefore impacts your credit utilization ratio I mentioned earlier. Closing one account should have a minimal impact on your score but closing multiple cards within a short period of time can have result in a material drop, especially if you have outstanding balances on other cards. If you want to close out a few accounts, there are a couple of factors to consider. Look to close cards with annual fees that aren’t justified by the benefits or cards that are relatively new. A longer credit history help improves your score so if deciding between an older account and a newer one, close the latter.

Is it beneficial to maintain a balance every month?

It’s a common misconception that carrying a balance helps build your credit. While consistent use of credit is necessary, an outstanding balance is not. Remember, potential creditors are looking at your report to see how likely you are to pay back your debt so a history of paying back your balances every month will only help. In addition, an ongoing balance will result in unnecessary interest charges and a higher credit utilization ratio – one of the main factors of your credit score.

Another (slightly morbid!) justification I have heard for carrying a balance is that it makes sense to die with a credit card balance since the credit card company will write-off the debt. This is only true if you have absolutely no assets, otherwise the lender has the right to go after your assets in order to recover any outstanding debt.

There are many nuances and there’s certainly no magic formula – different credit situations work for different people. However, if you make your payments on time, maintain low or no balances on your revolving credit (credit cards) and check your report for mistakes on a regular basis you should have no problem building and maintaining a good score.

FICO is a registered trademark of Fair Isaac Corporation.