Until the story of the hunt is told by the lion, the tale of the hunt will always glorify the hunter.

– African proverb

The political divisiveness that has percolated since the 2016 election continues to suggest that our ability to view issues from other perspectives is challenged. And that’s a problem not just for our politics, but for our financial lives as well.

The allure of a narrow, one-sided perspective is in the simplicity and focus of its message. But that doesn’t make it accurate. As financial advisors, we spend a lot of time reading and thinking about cognitive bias, in other words, how our hunting stories” may overstate our upside at the expense of the outsider’s objective interpretation.

Consider the following, as highlighted by the Wall Street Journal: Studies have shown that people remember voting regularly in national elections even when they haven’t cast a ballot in at least six years and that 71% of students who earned D grades in high school later recall getting higher marks[i].

If our memories can distort simple facts, how do they treat more complex and emotional topics like money? Where do our vulnerabilities lie?

I would argue that, at least in part, it’s in the way we remember our financial stories. We are prone to remember past losses as being smaller and gains as being far greater in magnitude. You see a lot more investment news venerating investment hunting” via speculative stock picks and market calls that proved right. You don’t often read a mea culpa from the fund manager who bet the farm and lost.

Which leads me to the following: it’s hard to really, truly remember the Great Recession (or the dot-com crash, or the savings & loan crisis, etc.) and how those portfolio losses made you feel.

Last month marked ten years since the collapse of Lehman Brothers. Rich and I often remind ourselves of how harrowing the days before and after that event were. But the truth is, we likely don’t remember the fear and anxiety so well now that we have perfect hindsight. People today are more apt to talk about the buying opportunity” of 2009 than anything else.

That’s even more so the case because things look very different today: markets have been more volatile of late, but still dance near all-time highs as the US economy continues to grow and unemployment drops to record lows. We are in the second longest economic expansion of modern times. History tells us that eventually things will take a turn for the worse and another recession will come.

I can’t say that’s coming soon or how severe it will be (and neither can anyone else if they’re being honest), but I do know that if and when it does arrive, it will have been a long time since investors have had to weather such challenges.

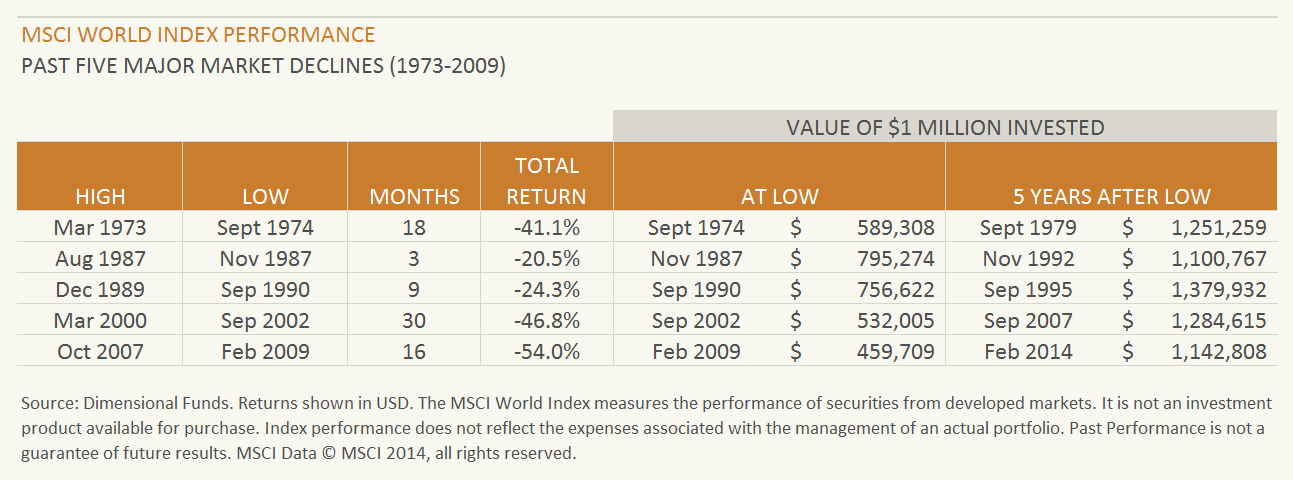

If you look back to the 1970s, the MSCI World Index experienced a downturn in excess of 20% every eight years on average, with the index declines ranging from 20.5% to 54.0% and lasting from three to 30 thirty months. Take a moment to reflect on the chart below. This is not meant to provoke fear. Just perspective.

Managing your expectations around market downturns will make you far more likely to have a good story in the next cycle. Take advantage of the relative calm waters now to talk to your advisors, check in with your financial plan, and rebalance your portfolio to take profits as appropriate. Try in earnest to consider the perspective of the lion, not just the glory of the hunter.

[i] Zweig, Jason. You’re Not as Good an Investor as You Think You Are.” The Wall Street Journal, Dow Jones & Company, 22 Feb. 2013